The intersection of physical cash and decentralized digital finance has created a lucrative playground for sophisticated bad actors, leaving state regulators scrambling to patch structural vulnerabilities. While traditional banking systems utilize decades of established security protocols, the rise of cryptocurrency kiosks—commonly known as Bitcoin ATMs—has bypassed these hurdles, allowing criminals to siphon hundreds of millions of dollars from unsuspecting citizens. This review examines the current legislative and technical attempts to bridge this security gap, focusing on how new oversight mechanisms aim to transform these machines from high-risk vulnerabilities into secure financial tools.

Introduction to Cryptocurrency Kiosk Technology and Oversight

Cryptocurrency kiosks serve as physical gateways that bridge the gap between tangible currency and the digital asset market. At their core, these machines function as automated teller interfaces where users can deposit cash to receive digital tokens, or vice versa. Unlike traditional ATMs, which are tethered to a centralized banking infrastructure and strict federal oversight, many early kiosks operated in a regulatory gray area. This lack of initial standardization allowed for a rapid, unchecked expansion of the hardware across convenience stores and gas stations, providing an “off-ramp” for illicit funds that is difficult for law enforcement to track.

The technology has evolved from simple transaction nodes into complex systems that must now integrate biometric scanning, real-time blockchain monitoring, and identity verification. As the digital landscape becomes more integrated with daily life, the oversight of these devices has moved from being a niche financial concern to a primary focus for state-level consumer protection agencies. The emergence of specialized legislation marks a shift toward treating these machines as high-stakes financial hubs rather than mere novelty dispensers, necessitating a complete overhaul of their operating software and physical usage protocols.

Core Mechanisms of Legislative and Technical Protection

Mandatory Licensing and Financial Oversight

One of the most significant shifts in the regulation of this technology is the transition toward mandatory money transmitter licensing. By requiring kiosk operators to obtain official state certification, regulators are effectively forcing a “Wild West” industry to adopt the same rigorous compliance standards as major commercial banks. This means that every transaction processed through a kiosk is now subject to a paper trail that state financial authorities can audit. The significance of this change lies in its ability to weed out smaller, undercapitalized operators who lack the technical infrastructure to support high-level security, thereby consolidating the market among companies capable of maintaining strict safety standards.

Beyond the legal paperwork, licensing mandates the implementation of advanced reporting software that flags suspicious transaction patterns. This architectural shift ensures that the software is not just processing data but actively analyzing the legitimacy of the user’s intent. For instance, when a license is tied to performance, operators are incentivized to integrate “velocity limits” that prevent large, rapid-fire transactions—a common hallmark of coercive scams. This regulatory pressure acts as a catalyst for better software engineering, pushing the industry toward a baseline of safety that was previously ignored in favor of higher profit margins and faster transaction speeds.

Real-Time Fraud Detection and User Verification

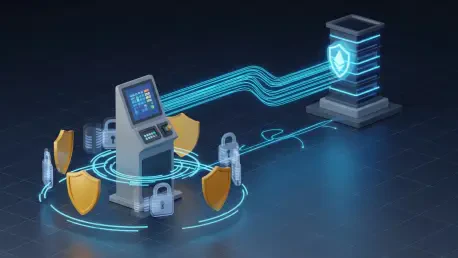

Modern kiosks are no longer just “dumb terminals” that accept cash; they are becoming sophisticated diagnostic tools equipped with identity verification (IDV) technology. High-performance units now require users to scan government-issued identification and undergo facial recognition checks before a single dollar can be deposited. This technical layer serves a dual purpose: it creates a definitive link between a physical person and a digital wallet, and it acts as a psychological deterrent for scammers who prefer anonymity. By integrating these features directly into the hardware, operators can cross-reference user data against global watchlists in milliseconds.

Moreover, the latest generation of kiosk software includes interactive fraud detection prompts that require users to answer specific questions before completing a transfer. If a user indicates they are sending money to a third party or are acting under the direction of a caller, the machine is programmed to terminate the session immediately. This real-time intervention is crucial because it disrupts the coercive cycle used by fraudsters, who often keep victims on the phone to guide them through the process. By forcing a break in the interaction, the technology creates a “cooling-off” period that can save a victim’s life savings during the most critical moments of the scam.

Emerging Trends in Digital Asset Regulation

The landscape is currently shifting toward a more aggressive, data-driven approach to consumer safety. A prominent trend involves the use of artificial intelligence to analyze blockchain addresses in real-time, allowing kiosks to block transfers to known criminal wallets before the transaction is even broadcast to the network. Instead of reacting to fraud after it happens, the industry is moving toward predictive prevention. This shift is influenced by a growing demand for “safe-haven” digital assets, where the average consumer expects the same level of protection from a crypto kiosk that they would receive at a traditional credit union.

Additionally, there is a burgeoning movement toward “store-level intervention,” where the physical location of the kiosk plays a role in its security. Some jurisdictions are exploring rules that empower store employees to intervene if they see a customer acting suspiciously while on a phone call. This trend represents a hybrid approach where technical safeguards are reinforced by human observation. As digital assets become more mainstream, the industry is moving away from the “code is law” mentality, acknowledging that human-centric vulnerabilities require human-centric solutions and more localized oversight.

Real-World Applications and Sector Deployment

In the retail sector, cryptocurrency kiosks are frequently deployed in neighborhoods where traditional banking services are scarce, serving as a primary entry point for the “underbanked” population. For these users, the kiosk is not a speculative tool but a functional utility for paying bills or sending remittances in a digital-first economy. In these environments, the deployment of highly regulated machines ensures that vulnerable populations are not exploited by predatory operators. This sector-specific usage highlights the dual nature of the technology as both a tool for financial inclusion and a target for criminal exploitation.

Furthermore, the integration of these kiosks into large-scale transportation hubs and major retail chains has forced a standardization of the user experience. By deploying machines in high-traffic, well-monitored environments, operators can leverage existing physical security—like CCTV and security guards—to complement the internal software protections. This deployment strategy makes it much harder for scammers to direct victims to a secluded machine where they can be coerced without interruption. The trend is clearly moving toward “high-visibility” deployments that favor transparency over the clandestine operations of the past.

Challenges and Technical Hurdles in Fraud Prevention

The primary technical hurdle remains the irreversible nature of the blockchain itself. Once a transaction is confirmed on the ledger, no amount of regulation can “undo” the transfer, making the prevention phase the only viable point of defense. This creates a high-pressure environment for software developers who must create systems that are foolproof but not so restrictive that they alienate legitimate users. Balancing the need for “friction” in the transaction process—to stop scams—against the demand for a seamless user experience is an ongoing struggle that often results in technical compromises.

Moreover, the regulatory landscape is fragmented, with different states and countries applying vastly different rules to kiosk operation. This lack of a unified global standard allows scammers to route funds through jurisdictions with weaker oversight, rendering local state-level protections less effective once the digital assets leave the immediate network. Technical development is currently focused on creating “inter-operable blacklists” that share data across different kiosk networks and jurisdictions, but the speed of legislative change often lags behind the rapid iterations of criminal tactics.

Future Outlook and Technological Trajectory

Looking ahead, the trajectory of cryptocurrency kiosk technology is headed toward deep integration with central bank digital currencies (CBDCs) and more robust decentralized identity (DID) frameworks. We can expect to see machines that do not just facilitate trades but act as comprehensive financial health hubs. These future units will likely incorporate advanced biometrics that can detect signs of stress or coercion in a user’s voice or gait, using AI-driven behavioral analysis to pause transactions automatically. This evolution will move the kiosks away from being standalone hardware and toward being nodes in a broader, safer financial ecosystem.

Furthermore, the “social” aspect of regulation will likely expand, with kiosks becoming more interconnected with local law enforcement databases. This would allow for immediate “welfare checks” if a machine detects a high-risk transaction involving a senior citizen or another vulnerable demographic. As the technology matures, the focus will shift from simply allowing access to crypto to ensuring that every entry point into the digital economy is fortified with multiple layers of defense. The long-term impact will be a more resilient financial infrastructure that respects the privacy of users while proactively neutralizing the threats posed by anonymous bad actors.

Assessment of the Regulatory Landscape

The review of the current regulatory environment revealed that the era of the unregulated cryptocurrency kiosk is effectively over. Legislators and technology developers have successfully identified the primary vectors of fraud—specifically the anonymity and speed of transactions—and implemented countermeasures that provide a necessary buffer for the consumer. While the technological solutions are not yet perfect, the mandatory licensing and enhanced identity verification protocols have created a significantly higher barrier to entry for criminals. The industry has shown a surprising willingness to adapt, recognizing that long-term survival depends on public trust and systemic legitimacy.

The proactive steps taken in recent years effectively transformed a high-risk financial instrument into a much safer gateway for the digital age. By focusing on point-of-sale intervention and real-time blockchain analysis, regulators moved beyond a reactive stance and established a framework that prioritizes the safety of the user’s assets over the raw efficiency of the transaction. Ultimately, the successful deployment of these safeguards proved that technological innovation and consumer protection are not mutually exclusive but are instead the twin pillars of a mature financial sector. This evolution successfully laid the groundwork for a more secure and transparent digital future for all participants.